Please see below today’s Daily Investment Bulletin from Brooks Macdonald, which was received this morning, 06/06/2024:

What has happened

Ahead of an expected interest rate cut from the European Central Bank likely later today, the Bank of Canada (BoC) has got there before it. Yesterday, the BoC became the first central bank out of the so-called ‘G7’ group of leading economic nations to cut its interest rates in the current monetary policy cycle, cutting by 25 basis points to 4.75%. Not only that, the BoC governor Macklem said yesterday that it was “reasonable to expect further cuts”. Elsewhere, economic confidence in markets returned on Wednesday with US services industry survey data out that was stronger than expected. In marked contrast to the manufacturing data earlier in the week. US services Purchasing Managers Index (PMI) from the Institute for Supply Management jumped 4.4 points month-on-month to 53.8. It was well above market estimates and was the highest reading in 9 months. Equity markets were buoyed by the better data with gains led by tech stocks, while government bond yields generally edged lower.

Nvidia reaches another milestone

Nvidia, the US megacap technology semi-conductor chip designer has hit another milestone. The poster child for the generative Artificial Intelligence (AI) boom, Nvidia’s share price was up +5.16% yesterday in US$ terms. With it, Nvidia narrowly overtook Apple to become the second largest quoted company in the US, with a market capitalisation of US$ 3.012 trillion, versus Apple’s US$ 3.003 trillion. For context, Microsoft is still number one with a market capitalisation of US$ 3.151 trillion. The latest surge in Nvidia’s share price has come about following news over the past few days that the company plans to upgrade its AI technology every year, announcing new generation chips in development earmarked for launches in 2025 and 2026. Key to the latest enthusiasm around the stock, CEO Huang is looking to broaden the company’s customer base beyond the handful of cloud-computing tech giants that have hitherto generated much of its sales.

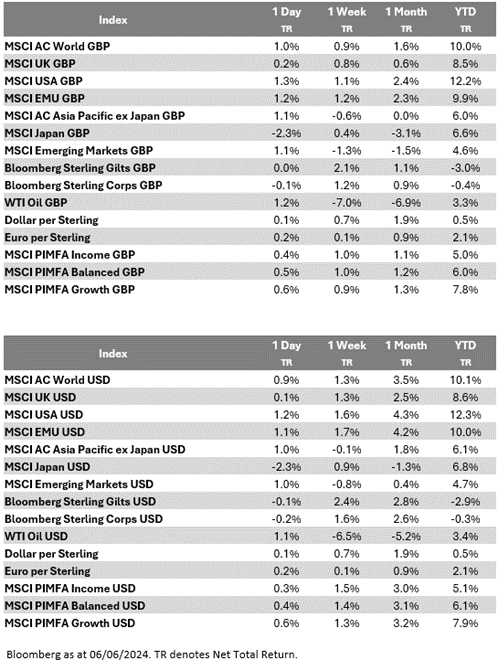

Oil prices see supply headwinds

Although the oil price saw a small bounce yesterday, it has dropped over the past week. Driving the fall was the latest OPEC+ meeting last weekend (the Organization of the Petroleum Exporting Countries plus non-OPEC members including Russia). Previously, OPEC+ members have been curbing output by a total of 5.86 million barrels per day (mbpd), or about 5.7% of global demand. At their latest meeting however, while OPEC+ agreed to extend 3.66 mbpd of cuts until the end of 2025, it said it would only prolong cuts of 2.2mbpd by three months until the end of September 2024. After September, OPEC+ plans to gradually phase out the cuts of 2.2mbpd over the course of a year from October 2024 to September 2025. That incremental supply is being seen as a headwind for prices and could signal some weakening in resolve amongst OPEC+ members to continue their supply curb discipline.

What does Brooks Macdonald think

Regular readers could be forgiven for thinking that it is not a Daily Investment Bulletin without mention somewhere about inflation! Over in Asia, inflation data out last month from Japan suggests that the recent recovery in prices, something which the Bank of Japan (BoJ) has hitherto been trying to engineer, is at risk. Japan’s so called ‘core-core’ Consumer Price Index (CPI) annual inflation, which exes out both fresh food and energy prices, dropped for the eighth month in a row in April. At an annual rate of +2.4%, it was the slowest inflation pace since September 2022, and not that far from the central bank’s 2% inflation target. For Japan’s central bank, there is a desire to try to normalise interest rates higher, after ending negative rates earlier this year. Should inflation rates continue to weaken, that could curtail the BoJ’s room for hiking, and risk putting yet more pressure on an already weak Japanese Yen currency this year.

Please continue to check our blog content for advice, planning issues and the latest investment, market and economic updates from leading investment houses.

Andrew Lloyd DipPFS

06/06/2024