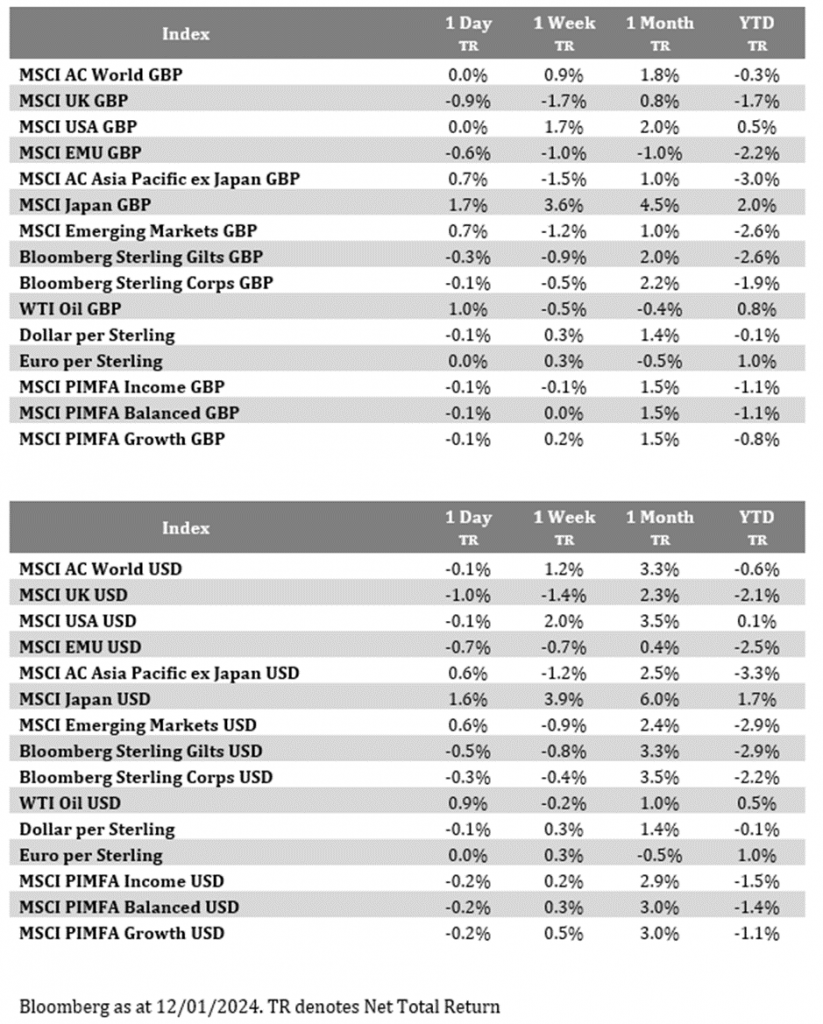

Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ providing a brief analysis of the key factors currently affecting global markets. Received this morning – 12/01/2024

What has happened?

Overnight the news that the US and UK have launched air strikes on Houthi rebels in Yemen is the main geopolitical story, however yesterday’s trading session was dominated by the US CPI release. US equity markets initially suffered after CPI came in above market expectations, however those losses were ultimately erased for the index to close only a few basis points lower.

Houthi air strikes

President Biden announced the strikes overnight saying that he would ‘not hesitate to direct further measures to protect our people and the free flow of international commerce as necessary.’ Oil prices rose as a result of this action and the market will also keep a close eye on container freight costs which will have inflationary impacts if they remain elevated.

US CPI

Starting with CPI, the monthly and annual headline CPI figures both surprised to the upside by 0.1%, meaning that the monthly figure expanded by 0.3%. For core CPI, the month-on-month expansion was also 0.3%, but that was in line with market expectations, although the year-on-year number fell less than hoped. The CPI readings were not disastrous for the soft landing narrative but continue to suggest that it will prove difficult to shift some of the stickier CPI subcomponents. In terms of those components, shelter is still running at 0.46% month-on-month which is important given its weight in the CPI basket. Interestingly, the PCE inflation measure, which the Fed officially targets, has a lower proportion allocated to shelter so may see less stickiness from this driver.

What does Brooks Macdonald think?

One of the logics behind the market rally later in the session was the realisation that if PCE continues to fall, despite CPI remaining sticky, this could give the US Federal Reserve the justification to cut interest rates should it want to. A surprising outcome from the day was the market’s expectations around a Fed interest rate cut by March which actually increased above a three-quarter percentage point probability. This occurred despite Fed speakers continuing to push back against such a certainty, with President Mester saying ‘I think March is probably too early in my estimate for a rate decline because I think we need to see some more evidence.’

Please continue to check our Blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

12th January 2024