Please see below, Brooks Macdonald’s ‘Daily Investment Bulletin’ which provides a brief analysis of global investment markets. Received this morning – 22/09/2023

What has happened?

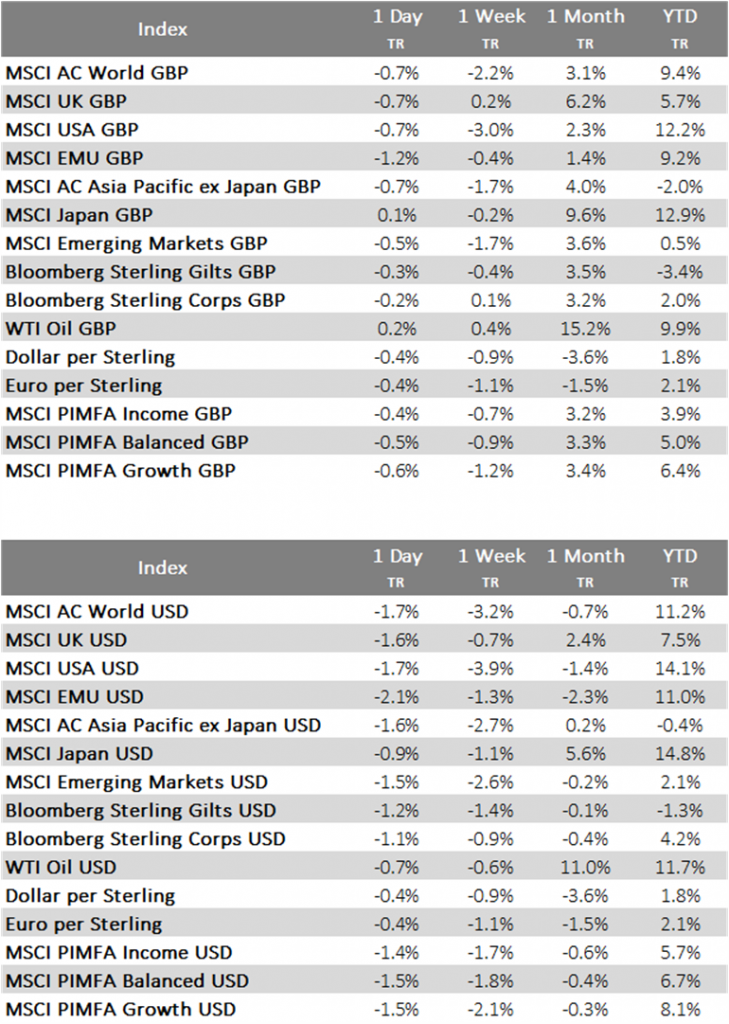

Both equity prices and bond prices sold off yesterday – the weakness driven by a higher-for-longer interest rate message from central banks this week, as well as better US weekly jobless claims data on Thursday pointing to a still-resilient US jobs market. US longer-dated bond yields hit new highs for the cycle, with the US-10year Treasury yield at one point over edging above 4.5% in trading overnight, which is the first time that has happened since 2007. Meanwhile the US 10yr real yield, up 6.6bps yesterday hit a post-2009 high of 2.11%. Earlier on Thursday, the Bank of England (BoE) narrowly voted 5-to-4 in favour of keeping rates on hold. Of the 9 MPC (Monetary Policy Committee) members, 5 voted for a pause, versus 4 voting for a 25bps hike. This marked the first time the BoE has left rates unchanged in almost 2 years, since November 2021. With markets reading the BoE decision as effectively supporting a higher-for-longer rate outlook as opposed to an even-higher-but-shorter peak, yields on UK government bond gilts rose across the maturity curve, with bond prices falling. In interest-rate derivative markets yesterday afternoon, peak rates were expected to only be around 18bps higher than now, so markets were no longer fully pricing in any more UK rate hikes this cycle.

Bank of England calls time on its 14-meeting rate hike streak

While the BoE’s pause mirrored the US Federal Reserve (Fed) the day before, there the similarity ends. While the Fed delivered a hawkish pause, it did so from a relatively more constructive backdrop, having doubled its real (constant prices) GDP outlook for 2023, while cutting its unemployment rate forecasts. For the BoE, its own pause arguably reflected having to balance inflation risks versus a more cautious economic picture – the BoE on Thursday cut its estimate for UK real Q3 GDP quarter-on-quarter growth from 0.4% to just 0.1% and said that ‘underlying growth was also likely to be weaker’ for the 2H of 2023. Perhaps a little ominously, the BoE also noted that ahead of its rate decision, it had had an early look at the flash UK PMIs (purchasing manager indices) for September which have only just come out this morning at the time of writing – as it turns out, both UK manufacturing and services remain in contractionary territory (with readings under 50), although services is weaker month-on-month, whereas manufacturing is a little better.

Bank of Japan keeps policy unchanged

As largely expected, the Bank of Japan (BoJ) used its latest meeting earlier this morning to keep all its policy settings unchanged. By a unanimous vote, there was no change to its short-term -0.1% negative interest rate policy setting, and no change to its guidance for the 10-year government bond yield target at ‘around zero’. As BoJ Governor Ueda said at the subsequent press conference earlier, “We have yet to foresee inflation stably and sustainably achieve our price target. That’s why we must patiently maintain ultra-loose monetary policy”, adding that “since we published the July outlook report, inflation isn’t overshooting sharply, but it’s not slowing as much as we expected.” Not surprisingly, in currency markets the Japanese Yen has weakened versus the dollar post the announcement. Earlier, the latest Japan all-items CPI (Consumer Price Index) annual inflation print for August came in at 3.2%, the lowest reading for 3 months, down slightly from 3.3% in July, and versus markets which had been expecting a flat 3.3% number. Meanwhile, core CPI (measured in Japan by excluding fresh food but still including energy) was 3.1% year-on-year.

What does Brooks Macdonald think?

The narrowness of the Bank of England vote to pause interest rates highlights the uncertainty around the economic outlook. We have yet to see the full impact of the cumulative 515bps of UK central bank rate hikes since December 2021, given interest rates work with around a lag of 18months or so for the full impact to reach the wider economy. That the BoE again used the phrase for keeping interest rates “sufficiently restrictive for sufficiently long” suggests that it is still keen to temper rate cut hopes anytime soon. All in all, the BoE’s communications seem to be in line with other central banks in distinguishing between an interest rate ‘pause’ and an outright ‘pivot’.

Please continue to check our blog content for advice and planning issues and the latest investment, markets and economic updates from leading investment houses.

Alex Kitteringham

22nd September 2023