Invesco give a good overview of markets in their weekly Performance Update issued today (14/04/2020) below:

With the early stages of a severe winter hitting the global economy, financial markets have decided it’s spring, preferring to focus on the green shoots of further central bank (particularly from the Federal Reserve) and government support (the EU finally came up with a €500bn package), as well as occasional snippets of good news on the coronavirus front. Consequently it was very much risk-on last week with some significant upward moves in both equity and credit markets.

Global equities had their strongest week (+10%) since 2008, but the real standout in Developed Markets was the performance of the FTSE 250 (UK Midcaps), which rose 16.3%, the biggest weekly gain since index data became available (1986). Global small caps had a record week too (+14%). Strong equity markets translated into declining volatility, although the VIX index (1m implied volatility of S&P 500) at 42 still remains at very elevated levels (it was at 14 when the S&P peaked on 19 Feb). In credit markets, HY, and US HY in particular, was boosted by the Federal Reserve expanding its asset purchase to include HY ETFs.

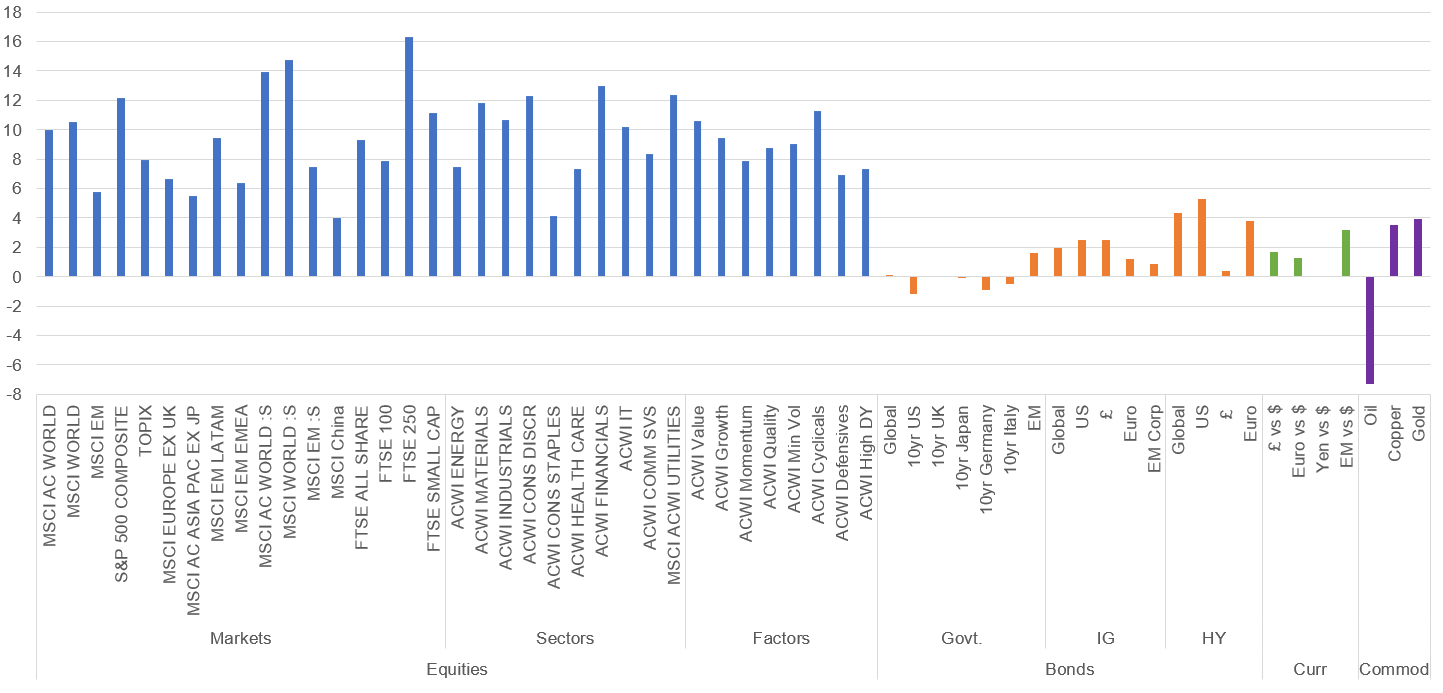

Market performance last week (%)

Past performance is not a guide to future returns. Sources: Datastream as at 13 April 2020. See important information for details of the indices used.1

Key observations on last week’s performance:

- Global equities rose sharply as highlighted earlier. DM (+10.6%) delivered almost double the return of EM (+5.8%) as US equities were particularly strong (+12.2%). A similar picture was seen in small caps (DM +14.7%, EM +7.5%). UK equities were also robust with the All Share having its best week’s performance since 2008, led by mid and small caps.

- At a sector level, risk-on invariably means that the more cyclical / value areas of the market outperform and last week was no exception. Financials, Consumer Discretionary and Materials were strong performers, while Consumer Staples and Communication Services were the main laggards. Exceptions to the rule were the defensive Utilities sector on the upside and Energy on the downside, although the latter probably exceeded expectations given the decline in the oil price. At a factor level there was little difference between Growth and Value, with the latter winning out marginally. Momentum and defensives were the weakest sectors.

- Developed Market government bond returns generally weakened at the margin on the back of a small uptick in yields, with the 10yr UST and Bund both rising 13bp. The 10yr Gilt yield was unchanged at 0.31%. EM sovereign bonds were the best performer, with yields falling 23bp.

- Global credit markets had a good week, particularly High Yield. Yields and spreads fell across the board, -30bp and -38bp respectively for IG and a more substantial -105bp and -122bp for HY. The lower the credit rating the better, with BBBs the best performer in IG and CCCs and below in HY. US credit outperformed on the back of Federal Reserve support.

- The risk-on backdrop weighed on the US$ with £, the Euro and EM currencies all appreciating versus the US$.

- Despite the OPEC+ agreement to cut oil production by 10mbd, along with additional support measures from the G20, making it overall the largest oil supply agreement in history, that was not seen as enough to offset the dramatic collapse in global demand. Consequently Brent fell -7.3% to just below $32. Copper, on the other hand, benefitted from the more optimistic tone in markets and the weaker US$. Gold too was strong, a beneficiary of a weaker US$, and at $1682 is at its highest level since early 2013.

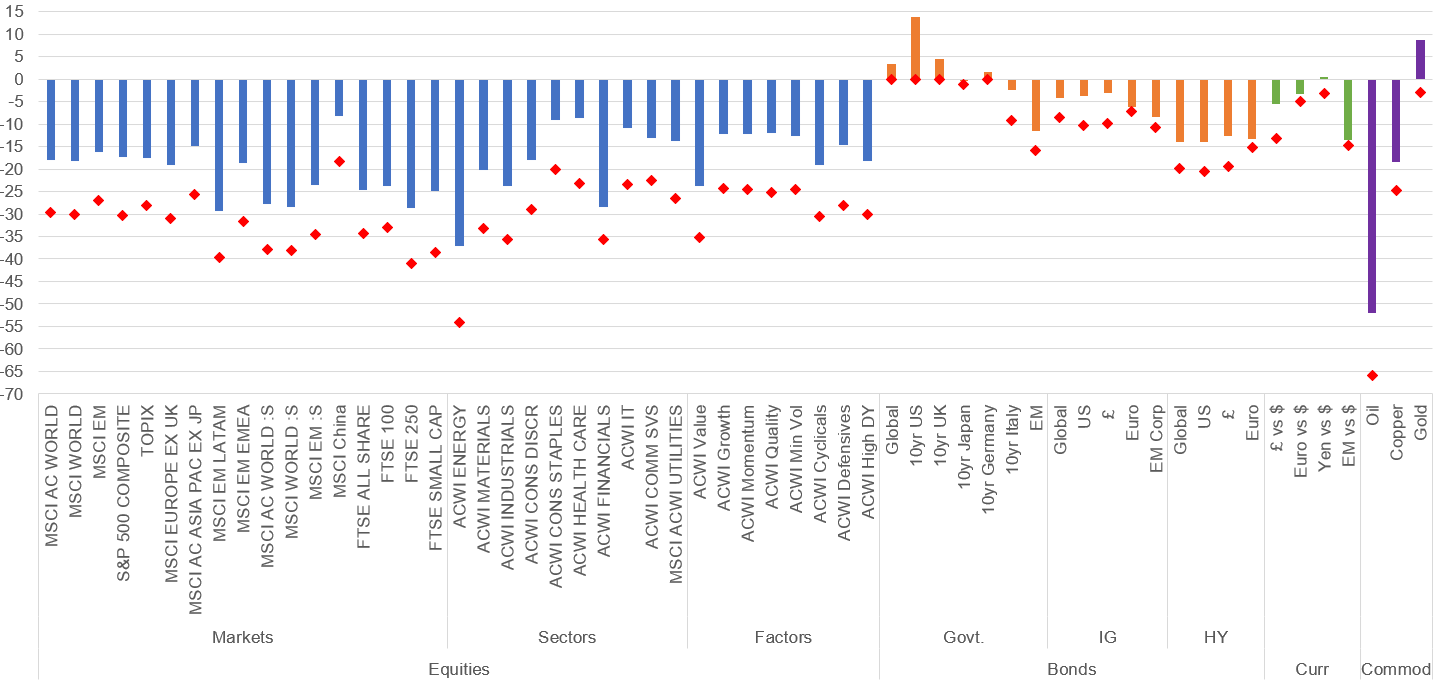

YTD market performance and YTD low (%)

Past performance is not a guide to future returns. Sources: Datastream as at 13 April 2020. See important information for details of the indices used.1

This week you will note that I have shown the maximum YTD drawdown as well. This is from the start of the year, not the peak to trough decline during the year so far.

Key observations on YTD performance:

- As the chart highlights it’s been a tough start to the year, but almost every asset class is now some way above their YTD lows, which were invariably seen in late March. There have been some significant rallies. The S&P 500 is +24.8% above its lows, the All Share +18.4% and US HY +12.4%.

- In equities EM (Asia best region) have marginally outperformed DM, with little performance differentiation between regions in the latter other than the UK, where the All Share is still down -24.5%. There has been a 10% performance divergence between large caps relative to small caps, a similar picture for Growth versus Value, while defensive sectors are ahead of cyclical ones by just under 5%.

- A fairly mixed bag from government bond markets. USTs have been the star performer with the 10yr UST YTM falling 119bp and returning 13.7%. Gilts have also been strong, with the 10yr down 52pts. EZ performance has been mixed. 10yr Bund yields (-15bp) have performed better than EZ peripheral bonds. The 10yr Italian BTP, for example, has seen yields rise +17bp. EM external sovereign yields have risen a massive 172bp, pushing returns down – 11.5% YTD.

- Despite the recent rally, credit markets remain firmly in negative territory. Global yields and spreads have widened dramatically (Yields IG +53bp HY +311bp, Spreads IG +144bp, HY +459bp). IG has outperformed HY materially. US and £ credit outperformed in IG, £ and Euro in HY. The weaker the credit rating the weaker the relative performance in both IG and HY.

- £ (-5.4%) and EM currencies (-13.4%) have been the main losers against the US$. Yen remains broadly unchanged, with the Euro slightly weaker.

- The oil price has halved (-51.8%). Economically sensitive Copper has also been very weak. Meanwhile gold (+8.6%) proves to be a robust safe haven.

Chart of the week: UK GfK consumer confidence survey

Source: Datastream as at 13 April 2020.

- GfK normally publishes its UK consumer confidence survey index once a month (at month end), having completed the survey during the first two weeks of the month.

- Last week they published a special flash survey, conducted in the last two weeks of March, to capture the impact of new restrictions on British life. It fell from -9 in the initial March survey to -34. This was not quite as low as the trough in the GFC (-40), but in terms of the economic outlook over the next 12m there was a new record low at -56 (GFC low -52).

- With unemployment expected to rise sharply, expectations on personal finances also slumped and are just above their GFC low (-17 vs -18).

- The current headline reading is consistent with household spending falling sharply. Last week’s car registrations give a foretaste of this. They are usually high in March due to the bi-annual plate change system. They fell 44.4%yoy from 458k in March 2019 to 255k in 2020, the lowest March number since the late 1990s.

Key economic data in the week ahead:

- Another relatively quiet week ahead in terms of economic news flow from the major economies.

- In the US, focus yet again will be on initial jobless claims (Thursday) after a rise of just under 17m in the past 3 weeks. Another “big” week is expected, with consensus at 5m. On Wednesday March’s retail sales will be published, where a record decline is expected. On that day a close eye will also be kept on the Federal Reserve’s Beige Book, a report published eight times per year ahead of the FOMC meeting (next one is 29 April), which provides anecdotal information on current economic conditions. Expect a material deterioration in the outlook.

- The highlight in China is the Q1 GDP report due on Friday. Remarkably for the second largest economy in the world, China manages to produce its final number (there are no revisions) well ahead of even provisional numbers for other major economies (the first reading for the US is not until 29 April). Consensus is for a -11.2%qoq decline and -6%yoy, by far and away the worst quarter ever experienced by the Chinese economy, reflecting the coronavirus lockdown shock. This will also impact trade numbers for March due on Tuesday. All a foretaste of what is to come in Europe and the US.

- A light week for data in the UK. With the BRC Retail Sales number for March (Thursday) we will get a first glimpse of how steep retail sales dropped, while the BoE Credit Condition Surveys on the same day will provide insight into the degree to which banks are ramping up supply of credit, given the expected jump in demand.

As you can see all focus is on the data coming out over the next c two weeks. We will experience ongoing volatility based on how Covid 19 is progressing/being controlled (how measures are working), the pathway out and the impact on global economies as outlined in the data we receive.

We need to remain invested as we are and be patient. Ongoing regular monthly contributions into pensions and investments will help over the medium to long term. Expect heightened volatility.

Steve Speed

14/04/2020