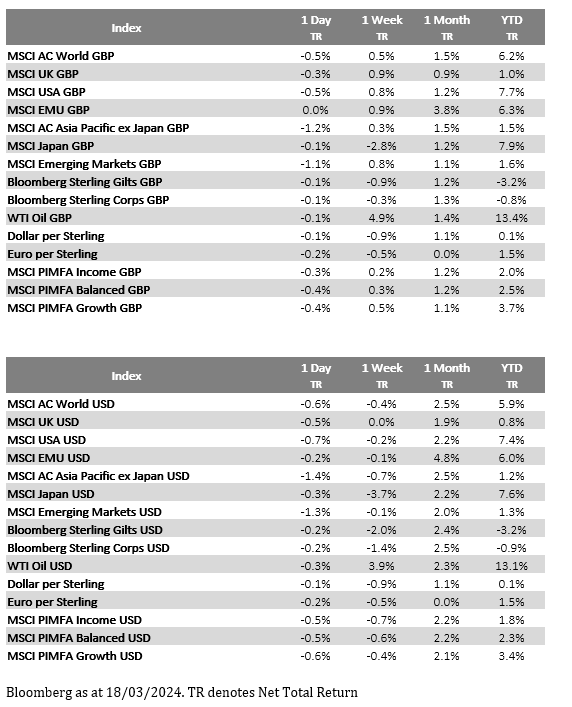

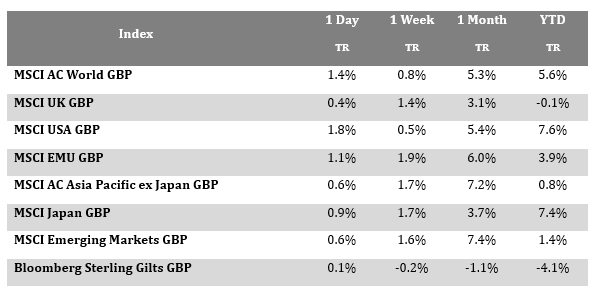

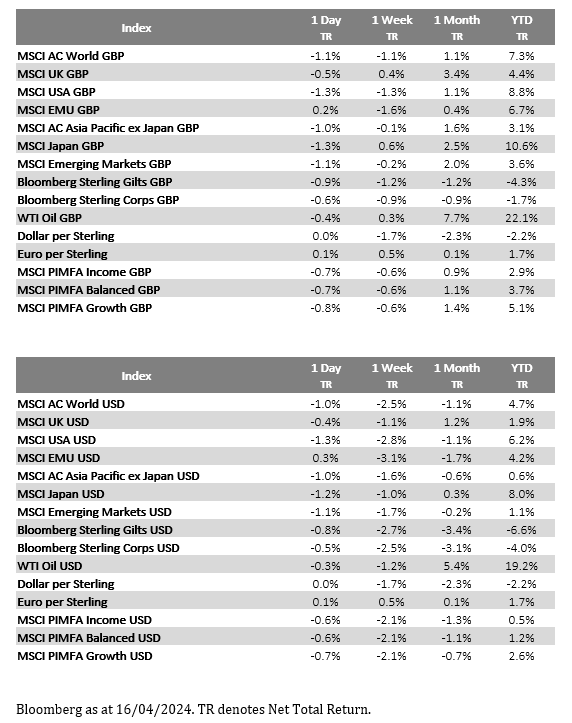

Please see below article received from Brooks Macdonald this morning, which provides a global market update following the recent attacks by Iran on Israel.

What has happened

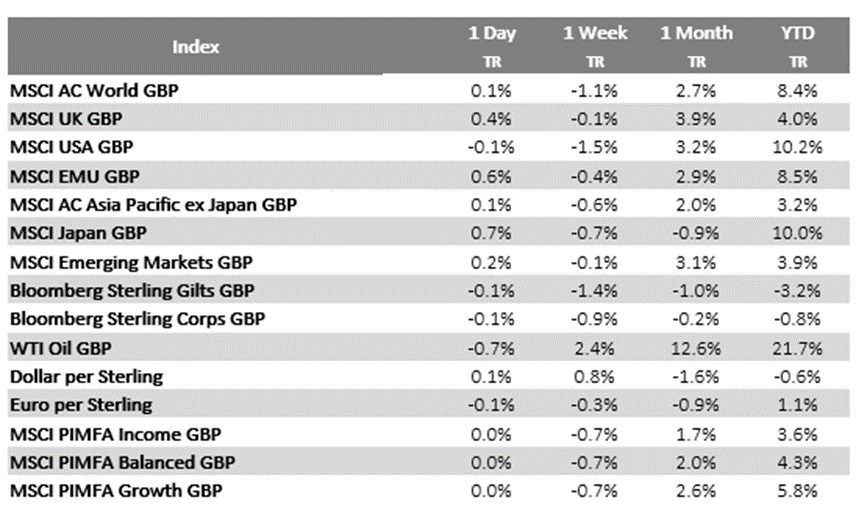

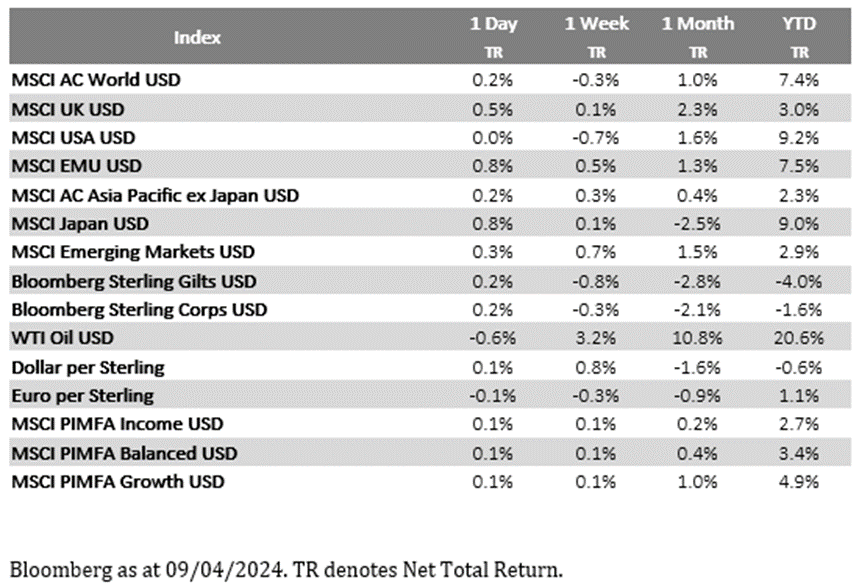

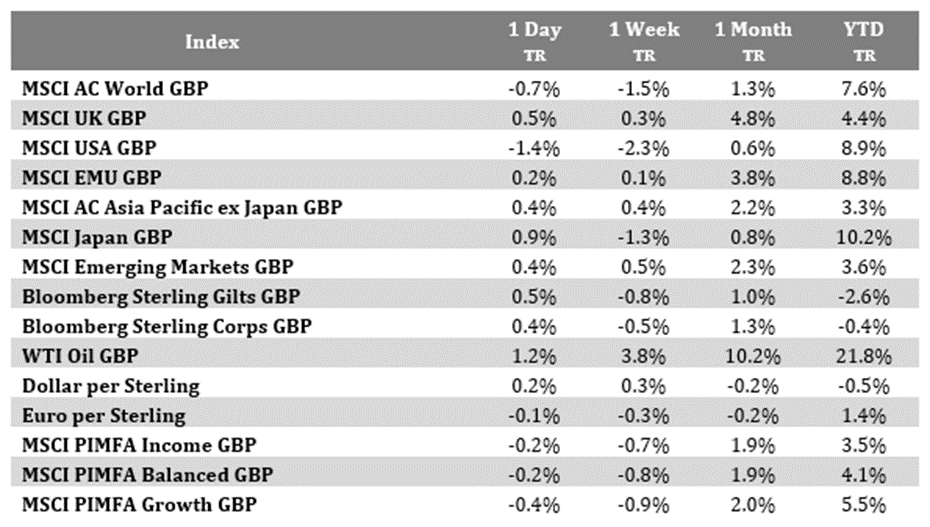

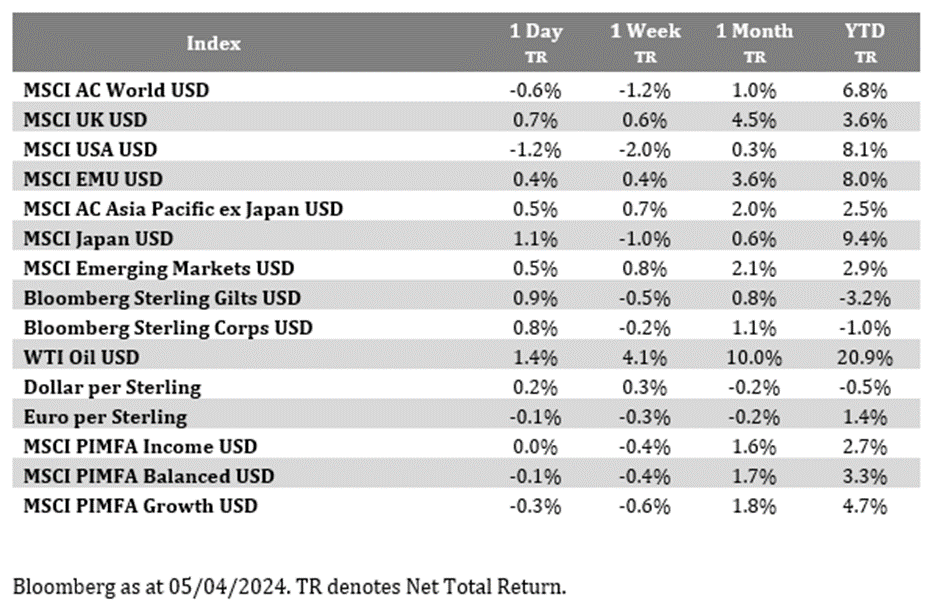

Following the unprecedented direct attacks by Iran on Israel over the past weekend, Middle East tensions continue to run high. There are still concerns around what Israel’s response is going to be, despite ongoing efforts by the US and allies to try to deescalate things. In equity markets, the US S&P500 index posted its weakest 2-day run on Monday since the US regional banking hiatus last March (falling -1.20% yesterday after -1.46% on Friday). The so-called ‘fear gauge’, the VIX volatility index (which is based off the S&P 500 equity index), rose +1.9 percentage points to 19.2 yesterday, seeing its sharpest two-day rise also since March last year. Corresponding with the risk-off mood, US 10-year Treasury government bond yields rose 8 basis points (bps) to their highest level in five months on Monday to 4.60%, and oil prices (Brent crude June futures) have edged higher this morning, trading back up above US$90 per barrel currently.

A mixed data bag from China

Overnight investors have received a rather mixed bag of economic data out from China, where it seems the economy’s strong start to 2024 is already losing steam. On the surface, China’s Gross Domestic Product (GDP) climbed +5.3% in Q1 2024 in year-on-year (YoY) terms, accelerating slightly from the previous quarter, where Q4 2023 was up 5.2% YoY, and ahead of expectations of 4.8%. However, much of the bounce came in the first two months of the year. In March, growth in retail sales slumped (growing +3.1% YoY, down from +5.5% YoY in February and below estimates looking for +4.8%), and industrial output decelerated below forecasts (+4.5% YoY in March, down from +7.0% in February and below estimates looking for +6.0%). Finally, in the all-important property sector, Chinese house prices continued to fall in March, dropping -2.7% YoY, and worse than the -1.9% drop in February, suggesting China’s property market is struggling to find a floor.

Allies try to deescalate Middle East tensions

All eyes are on the Middle East at the moment. Yesterday, a number of Western allies cautioned Israel against an escalation following Iran’s attacks at the weekend: French President Emmanuel Macron said, “we’re going to do everything we can to avoid flare-ups, and try to convince Israel that we shouldn’t respond by escalating, but rather by isolating Iran”; UK Foreign Secretary David Cameron said that “we’re saying very strongly that we don’t support a retaliatory strike”; and US President Joe Biden said the US “is committed to Israel’s security” and “to a ceasefire that will bring the hostages home and prevent the conflict from spreading beyond what it already has”. Against this, news website Axios reported yesterday that Israel’s defence minister Yoav Gallant told US Defence Secretary Lloyd Austin that Israel couldn’t allow ballistic missiles to be launched against it without a response – further it was reported by news channel CNN that Israel’s war cabinet reviewed military plans for a potential response in a meeting on Monday, without clarity on whether a decision had been taken.

What does Brooks Macdonald think China’s recovery has been somewhat unbalanced since pandemic restrictions were lifted at the tail-end of 2022 coming into the start of last year. While manufacturing is holding up, there is a continued real estate downturn which is weighing on confidence. Further, the hope that China can rely on adding to manufacturing, arguably adding to overcapacity there, in order to try to export itself out of its economic challenges is meeting somewhat protectionist resistance from other countries – the European Union having only recently initiated a raft of investigations against China, including an investigation into Chinese subsidies for electric vehicles. For China, it is simply down to the composite weights of the various sum of the parts of China’s economy. The pickup in the Q1 GDP numbers was almost entirely driven by public investment – in contrast, underperformance in production and private demand suggest China’s recovery is still on thin ice. Ultimately, such is the weight of China’s property sector as a share of GDP (some market estimates put property-related activities having in the past contributed as much as a c.30% share of China’s economy, roughly that for the US by comparison), that without significant intervention here, something China’s policy makers still appear loath to do, there is arguably not enough impetus elsewhere to give broader economic growth in China the so-called ‘escape velocity’ it really needs.

Please check in again with us shortly for further relevant content and market news.

Chloe

16/04/2024